Procurement teams ask three questions before any export programme moves: lead time, compliance, and how this gets paid. The first two we've covered elsewhere. This is the third, in full.

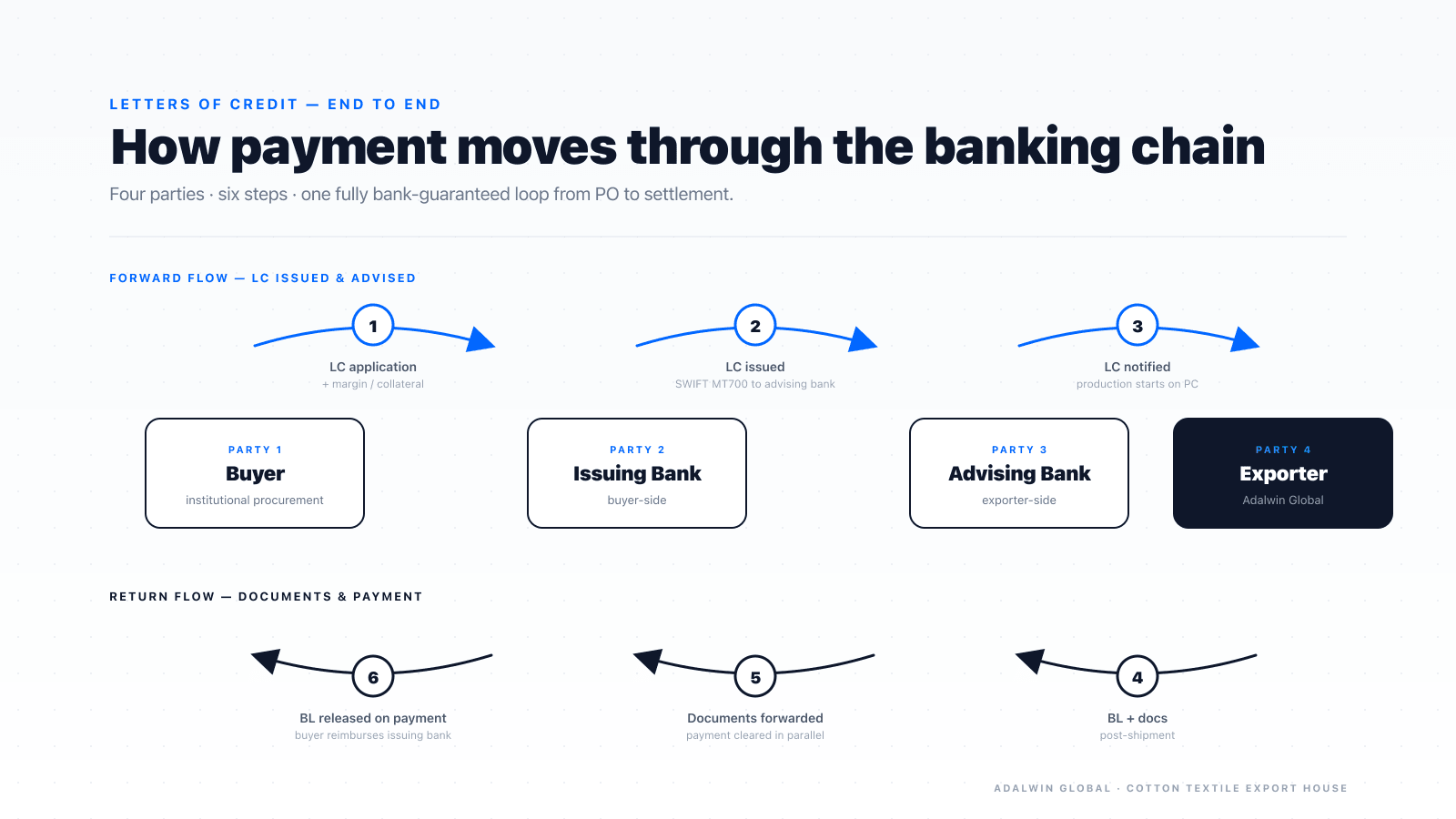

A container of cotton textiles leaves Mundra under a Letter of Credit, a Documents-against-Acceptance draft, or a TT wire. Each has a different risk profile, a different financing cost, and a different bank-side conversation. For institutional buyers placing orders against Adalwin Commerce™ LLP, knowing how this machinery actually works is the difference between a clean 60-day cycle and a stuck container.

What follows is the export finance stack from our side of the desk — the structures we operate under, the trade-offs, and the worked numbers behind each.

Two LC structures worth knowing

Transferable LC

A transferable LC originates with the buyer's bank and lands as a credit instrument the exporter can split — assigning a portion downstream to the manufacturer or supplier.

Worked example. The buyer issues a $100,000 transferable LC in our favour. We assign $80,000 to the mill carrying the programme so production starts on day one; $20,000 stays with us as the trade margin. The mill ships against its $80,000 sub-LC; we file our final invoice and the bank consolidates both into the $100,000 the buyer originally committed.

Two operational properties matter:

- Opaque on both sides — the buyer never sees the mill's price; the mill never sees the buyer's. The transfer is informational only to the banks.

- Liquidity for the mill — now holding a verifiable bank instrument, the mill can take the LC to its own bank and draw Packing Credit. This is how a new exporter with no banking history clears its first order.

Confirmed LC

When the buyer is in a country with political or currency-control risk that the buyer's bank itself won't underwrite, a third party — typically a global bank in New York, London or Singapore — adds its own commitment to the credit. The exporter then submits documents to the confirming bank and gets paid by it; the confirmer runs its own collection cycle against the issuer.

For Adalwin's seven buyer markets — USA, UK, EU, Germany, Middle East, Australia, Canada — vanilla irrevocable LCs are the norm. Confirmed LCs show up more often on Eastern European, African and certain Middle Eastern programmes.

Two drafts behind every LC

Every LC eventually settles via a draft — a payment instruction sent from the exporter's bank to the buyer's. There are two shapes, plus a hybrid.

Sight Draft — Documents against Payment (DP)

Cash on the table. The exporter sends the Bill of Lading plus a Sight Draft to the buyer's bank. The bank releases the BL only after the buyer pays. No payment, no container.

This is what large groups with strong banking relationships default to. It's the cleanest from the exporter's side: no credit exposure, no waiting period.

Usance / Time Draft — Documents against Acceptance (DA)

Buyer-friendly credit terms. The BL and a Usance Draft arrive at the buyer's bank, and the buyer signs the draft accepting a 30, 60 or 90-day credit period. The bank then releases the BL — but doesn't hold the buyer financially liable to pay. The bank just nudges the buyer on the due date.

The exporter is effectively extending an unsecured 30/60/90-day loan. For institutional buyers with track records this is fine. For new relationships, it carries real default risk.

Avalized Draft (the hybrid)

A risk-mitigated variant of the Usance Draft. The buyer's bank co-signs the draft, formally guaranteeing payment on the due date even if the buyer defaults. The signed draft goes back to the exporter's bank, which now holds a bank-backed promise rather than a corporate one.

The catch: there's still in-transit risk. If the buyer refuses receipt of goods or the political situation in the destination country deteriorates between draft acceptance and the due date, the surety can crumble. The standard solution is layering ECGC (Export Credit Guarantee Corporation of India) cover on top — it protects against political risk, buyer insolvency, and a range of in-transit and post-shipment failure modes.

Bill discounting — turning paper into working capital

A Usance Draft, Avalized or otherwise, is a 60-day promise. Cash is cash, but a promise of cash 60 days from now doesn't pay the mill's payroll today.

Bill discounting is the standard fix. The exporter sells the draft (or the accepted invoice) to their own bank at a discount; the bank pays today, then collects the full amount on the due date.

Worked example. A $100,000 receivable due in 60 days. The bank takes a $2,000 cut and pays $98,000 today. Whether $2,000 is reasonable depends on the prevailing SOFR-based rate and the bank's view of the buyer's credit.

Where the underlying is an Avalized Draft, the bank carries low risk and the discount is small. Where it's a plain Usance Draft, the bank wants either ECGC cover or post-shipment limits / collateral to absorb the downside. Without either, the discounting facility either doesn't get extended or comes with a punitive rate.

SOFR — the rate behind every number

The Secured Overnight Financing Rate, published by the New York Fed, is the international floating benchmark for USD lending. Most Indian export finance is priced as SOFR + a markup.

As of writing, SOFR sits around 3.6%. Indian banks typically add ~2.5%, putting Post-Shipment Credit at roughly 6.1% per annum.

Worked example. A $100,000 IOU due in 60 days, sold to the bank for discounting:

- 6.12% per annum on $100,000 = $6,120 in annual interest

- Daily run-rate: $6,120 ÷ 360 ≈ $17

- 60-day discount: $17 × 60 ≈ $1,020

The bank pays out $100,000 − $1,020 = $98,980 today. On day 60, the bank collects $100,000 from the buyer and books $1,020 as interest.

This is the linear maths. Everything from Packing Credit through Post-Shipment Credit through factoring runs the same equation; only the markup, the tenor and the principal change.

Pre-shipment and post-shipment credit

Pre-Shipment Credit / Packing Credit (PC)

Working capital for the exporter to fund production after receiving an LC or PO and before the container ships. Banks typically lend this at ~2.5% below the standard commercial rate, recognising it as export-priority lending.

Packing Credit is repaid in one of two ways. Either the exporter wires the bank back from settled cash, or it rolls automatically into Post-Shipment Credit once the container leaves.

Post-Shipment Credit (PSC)

Provided against a Usance LC or DP documents post-shipment. The bank writes off the existing Packing Credit balance, deducts the tenor interest (the 30/60/90-day discounting cost), and disburses the remainder.

Currency choice matters. Disbursing in USD at SOFR + markup is cheaper than converting to INR and borrowing at MCLR / EBLR rates. Some exporters also use matching — settling USD-denominated import payables directly out of receipt USD without converting, eliminating two FX cycles.

Recourse vs Non-recourse — who carries buyer-default risk

When the exporter sells a receivable to the bank, the contract specifies what happens if the buyer never pays. This is the difference between a clean exit and a contingent liability sitting on the exporter's books for sixty days.

Recourse

The discount or factoring arrangement is “with recourse” — if the buyer defaults, the bank turns to the exporter for the money. The advance that landed on day one becomes a loan on day sixty-one. Directors typically sign personal guarantees as part of the facility.

ECGC cover changes this materially. If the exporter holds ECGC cover and the buyer defaults, ECGC reimburses the bank up to the covered percentage (typically 80–90%); the exporter is only on the hook for the gap.

Non-Recourse

The receivable is sold outright. The bank or factoring company takes full collection risk. If the buyer defaults, that's the bank's loss, not the exporter's.

The interest is higher to compensate, but the exporter's balance sheet is clean from day one. For programmes the exporter wants to fully derisk — first-cycle orders with new buyers, for instance — non-recourse is structurally cleaner.

Factoring — recourse and non-recourse

Factoring is bill discounting's cousin. Instead of the exporter's own bank, a specialist factoring company buys the commercial invoice directly.

Recourse factoring

The factoring company advances 80% of the invoice value immediately. The remaining 20% lands when the buyer pays, less interest and a service fee (typically 0.1% – 0.5% of invoice value).

If the buyer defaults, the 80% advance turns into a loan against the exporter at the original SOFR + markup rate. Directors' personal guarantees serve as collateral.

Worked example. A $100,000 invoice. The factor advances $80,000 on day one. The buyer pays in full on day 60. The remaining $20,000 is settled after:

- Tenor interest at ~6.62% on $100,000 for 60 days ≈ $1,103

- Service fee ≈ $300

- Net second remittance ≈ $18,597

Non-recourse factoring

The factoring company takes the buyer's credit risk in full. 80% advance on day one, no recourse to the exporter if the buyer defaults. Service fee is higher (0.5% – 1.5%) and the tenor interest is around 1% higher to price in the buyer-risk transfer.

DGFT's interest subvention of 2.75% for non-recourse factoring closes much of that gap. The effective rate drops from ~6.12% to roughly 3.37%.

Worked example. Same $100,000 invoice. The non-recourse factor advances $80,000 on day one.

- Tenor interest: 3.37% × $100,000 × 60/365 ≈ $554

- Service fee at 1%: $1,000

- Total deductions: ≈ $1,554

- Final remittance to exporter (after buyer pays): ≈ $98,446

The exporter receives $80,000 immediately and ≈$18,446 once the buyer settles. The factoring company carries the default risk in the interim.

Commercial disputes — quality claims, dimension misfires, packaging defects — remain the exporter's responsibility. The factor only covers buyer-side financial failure, not seller-side performance issues. A commercial dispute caught by the buyer can force the exporter to wire back the 80% to the factor; failure to do so promptly attracts 10–12% penalty interest.

What this means for buyers procuring from Adalwin Global

This stack — LC, drafts, ECGC, discounting, factoring, recourse split — is the operating infrastructure behind every container Adalwin Global ships. For institutional procurement teams placing orders against Adalwin Commerce™ LLP, three implications matter.

- Payment terms are negotiable inside a defined envelope. Irrevocable LC at sight is standard for Fortune-500 retail and large hotel groups; TT against documents works for established mid-size buyers; Wise Business and PayPal Business clear in days for first-cycle sample orders. Open Account 30/60/90 is on the table only for buyers we've completed at least one full shipment cycle with — and where ECGC cover or Avalized Drafts can backstop the credit exposure.

- The price quoted is the landed cost, not a teaser. Programmes priced FOB JNPT or CIF destination include the cost of running this finance machinery. There are no surprise discounting markups or factoring fees added mid-contract.

- Buyer-side documentation discipline matters. A clean LC application — accurate Incoterms, correct port-of-discharge, complete beneficiary banking details, correct HS codes — clears the entire cycle without amendments. Each amendment adds 2–3 days and a $50–$100 bank fee. We brief buyers' procurement teams on LC drafting on request.

The headline: this isn't bureaucracy. It's the operating discipline that makes a 60-day cycle predictable for both sides.